What does the Truth in Lending Act Regulation Z required

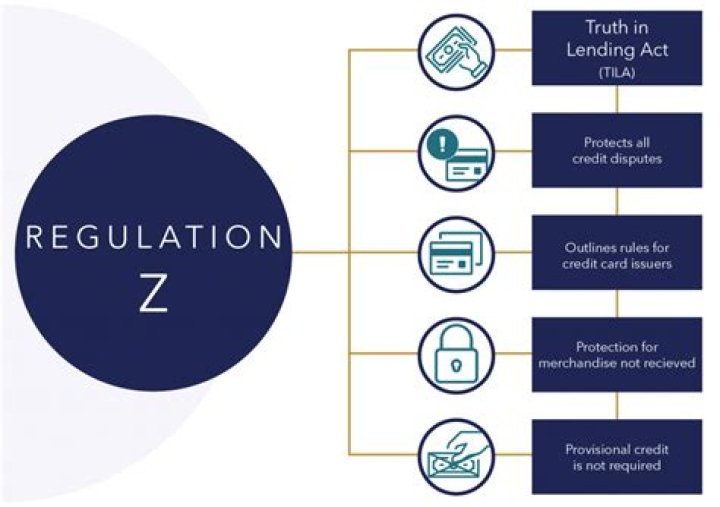

Regulation Z is a law that protects consumers from predatory lending practices. Also known as the Truth in Lending Act, the law requires lenders to disclose borrowing costs so consumers can make informed choices.

What does the Truth in Lending Act Regulation Z require quizlet?

Requires creditors to disclose key terms and costs to consumers for credit transactions through statements and fair advertising practices. Promotes the informed use of credit.

What is the Regulation Z of the Truth in Lending Act?

Regulation Z prohibits certain practices relating to payments made to compensate mortgage brokers and other loan originators. The goal of the amendments is to protect consumers in the mortgage market from unfair practices involving compensation paid to loan originators.

What does the Truth and Lending Act require?

The TILA requires lenders to disclose credit terms in a way that’s easy to understand, so consumers can confidently compare interest rates and conditions and make informed decisions. Because independent schools provide an educational service in exchange for compensation, they’re considered merchants.What are the requirements of Tila?

Lenders must provide a Truth in Lending (TIL) disclosure statement that includes information about the amount of your loan, the annual percentage rate (APR), finance charges (including application fees, late charges, prepayment penalties), a payment schedule and the total repayment amount over the lifetime of the loan.

Is a truth in lending statement required?

The federal Truth-in-Lending Act – or “TILA” for short – requires that borrowers receive written disclosures about important terms of credit before they are legally bound to pay the loan.

What does Regulation Z require a lender to disclose to a consumer?

The primary way the regulation protects consumers during the mortgage process is by eliminating a conflict of interest for mortgage brokers. … Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges.

What does the Truth in Lending Act of 1969 require lenders to do what is the APR and how does it fulfill the purpose of the act?

What Does the Truth in Lending Act Do? The Truth in Lending Act (TILA) helps protect consumers from unfair credit practices by requiring creditors and lenders to pre-disclose to borrowers certain terms, limitations, and provisions—such as the APR, duration of the loan, and the total costs—of a credit agreement or loan.Why is the Truth in Lending Act important?

The Truth in Lending Act (TILA) protects you against inaccurate and unfair credit billing and credit card practices. It requires lenders to provide you with loan cost information so that you can comparison shop for certain types of loans.

What is a Truth in Lending statement?A Truth-in-Lending Disclosure Statement provides information about the costs of your credit. … Your Truth-in-Lending form includes information about the cost of your mortgage loan, including your annual percentage rate (APR).

Article first time published onWhat are the two most important disclosures that appear on the Reg Z disclosure statement?

Reg Z requires disclosure of the finance charge and Annual Percentage Rate (APR) regardless of whether you are granting a revolving credit line or an installment loan. days after approval to give the applicant time to decide whether or not to accept.

How does the federal Truth in Lending Act applies to debt collection practices?

The Truth in Lending Act (TILA) protects consumers by requiring creditors to disclose certain information about finance charges, annual percentage rates, payment amount, and fees that may be charged to the consumer.

Why is APR required to be disclosed?

The APR, which must be disclosed in nearly all consumer credit transactions, is designed to take into account all relevant factors and to provide a uniform measure for comparing the cost of various credit transactions. The APR is a measure of the cost of credit, expressed as a nominal yearly rate.

What does a Truth in Lending Act disclosure statement look like?

What Does a Truth in Lending Disclosure Look Like? The cost of your credit as a yearly rate. The dollar amount the credit will cost you. The amount of credit provided to you on your behalf.

Who enforces Truth in Lending Act?

The Federal Trade Commission is authorized to enforce Regulation Z and TILA. Federal law also gives the Office of the Comptroller of the Currency the authority to order lenders to adjust and edit the accounts of consumers whose finance charges or annual percentage rate (APR) was inaccurately disclosed.

Which of the following must be disclosed according to Regulation Z?

Under these rules, lenders must disclose interest rates in writing, give borrowers the chance to cancel certain types of loans within a specified period, use clear language about loan and credit terms, and respond to complaints, among other provisions.

What is a real life example of the Truth in Lending Act?

One of the ways the TILA does that is by limiting the changes a lender can make to your loan or credit terms after you’re approved. For example, the TILA requires creditors to give you 45 days’ advance notice before increasing certain credit card fees.

When Should Truth in Lending disclosures be provided to the consumer?

According to the Consumer Financial Protection Bureau, you must be given a written TILA disclosure, before you become legally obligated to pay off the loan. The importance of seeing it before you are obligated cannot be overstated.

What are the requirements Reg Z imposes on loans expressly for education purposes?

Regulation Z consists of three disclosures provided to the borrowers of private education loans at specific intervals of the loan application and approval process. These disclosures are required for every private education loan a school or lender provides, and must contain special HEOA requirements and content.

How does the federal Truth in Lending Act apply to debt collection practices quizlet?

Truth in Lending Act requires sellers and lenders to dicslose credit terms or loan terms so that individuals can shop around for the best financing arrangements.

Does Truth in Lending apply commercial loans?

Truth-in-Lending Act (TILA) Generally, no. TILA does not apply to business-purpose loans (including loans to acquire, improve or maintain non-owner occupied rental property) or loans made to entities.

How do you read a Truth in Lending Disclosure?

- Annual Percentage Rate (APR) This reflects your yearly interest rate and origination fee.

- Finance Charge. This charge shows the total amount you’ll pay in interest, plus your origination fee. …

- Amount Financed. …

- Total of Payments.

When calculating the APR for a closing disclosure under Regulation Z Which of the following items would not be included?

Actual costs not retained by lenders (title fees, legal fees, closing costs, property taxes, appraisal fees, recording fees, notary fees, etc.) are not considered finance charges and are not included in the APR. You just studied 116 terms!

What is required to be disclosed on the privacy notice?

The Contents of the Privacy Notice Your notice must include, where it applies to you, the following information: Categories of information collected. For example, nonpublic personal information obtained from an application or a third party such as a consumer reporting agency. Categories of information disclosed.