Can a seller refuse FHA loan

Yes, a seller can refuse an FHA loan offer from a home buyer. You can refuse any offer that doesn’t meet your needs or expectations. Housing discrimination, on the other hand, is prohibited by law.

Why do some sellers refuse FHA loans?

Why Do Some Sellers Not Accept FHA Loans? Sellers want to be able to sell their home with as little frustration and cost to them as possible. Anything they believe may pose a risk to the perfect sale may send them running in the other direction.

Can you discriminate against an FHA loan?

The FHA also forbids discrimination based on race, color, religion, sex, national origin, handicaps, or familial status. That’s defined as children under 18 living with a parent or legal guardian, pregnant women, and people securing custody of children under 18.

How does FHA loan affect seller?

FHA loans attract buyers who might not have the cash savings for the closing costs out of pocket. FHA loans let the seller pick up as much as 6 percent of the value of the home to pay the buyer’s closing costs, making it easier for the buyer to afford the house.What happens if house doesn't appraise FHA?

When the appraisal comes in below the asking price, there are several things you can do: The homeowner / seller could reduce the selling price to match the appraised value. … You could get a loan for the appraised value (or a portion of it, minus your down payment) and then pay the remainder out of your own pocket.

Are FHA appraisals a problem?

FHA loans require that the home be appraised by an appraiser who meets high qualifications. The property condition is one of the biggest reasons why an FHA mortgage could be a problem for a home seller. … It will then become a condition of the loan that must be remedied before a final mortgage commitment is granted.

Why would a seller want a conventional loan?

Length of Time to Close. By and large, conventional loans simply tend to close faster. Less paperwork and fewer stipulations allow these mortgages to be processed more quickly, and many sellers find this to be an attractive bonus.

What are HUD violations?

Housing providers who refuse to rent or sell homes to people based on race, color, national origin, religion, sex, familial status, or disability are violating federal law, and HUD will vigorously pursue enforcement actions against them.Can my loan be denied at closing?

Can a mortgage loan be denied after closing? Though it’s rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. “It’s not unheard of that before the funds are transferred, it could fall apart,” Rueth said.

Can I sue the underwriter?Seeking Legal Help for Mortgage Underwriter Issues The underwriter plays a major role in the approval or rejection of the borrower’s application. … Your attorney can provide you with legal advice and can also represent you in court if you need to file a lawsuit.

Article first time published onCan a seller appeal an FHA appraisal?

The Department of Housing and Urban Development (HUD) oversees the FHA; both agencies can work with your lender to review the appraisal, and making the situation known to the agencies can speed up the appeals process.

Can seller back out if appraisal is low?

Can a seller back out after a low home appraisal? Only the buyer can back out of a contract if the home’s appraisal comes in too low. This also is dependent on the buyer having an appraisal clause in their purchase agreement.

How fast can a FHA loan close?

You can typically close on an FHA purchase or refinance within 30 days of submitting your loan application.

Whats better for the seller FHA or conventional?

There are two situations when a seller should choose a Conventional offer over an FHA offer. First, if the property has safety issues or things that need to be fixed, a Conventional appraisal will be less likely to point out those issues while an FHA appraiser will require those to be fixed prior to closing.

Do sellers prefer conventional or FHA?

“If there are multiple offers on a home, sellers tend to give preference to borrowers with conventional financing,” Yates said. Why is that? Sellers worry that if they accept an offer from a borrower with FHA financing, they’ll run into problems during both the home appraisal and home inspection processes.

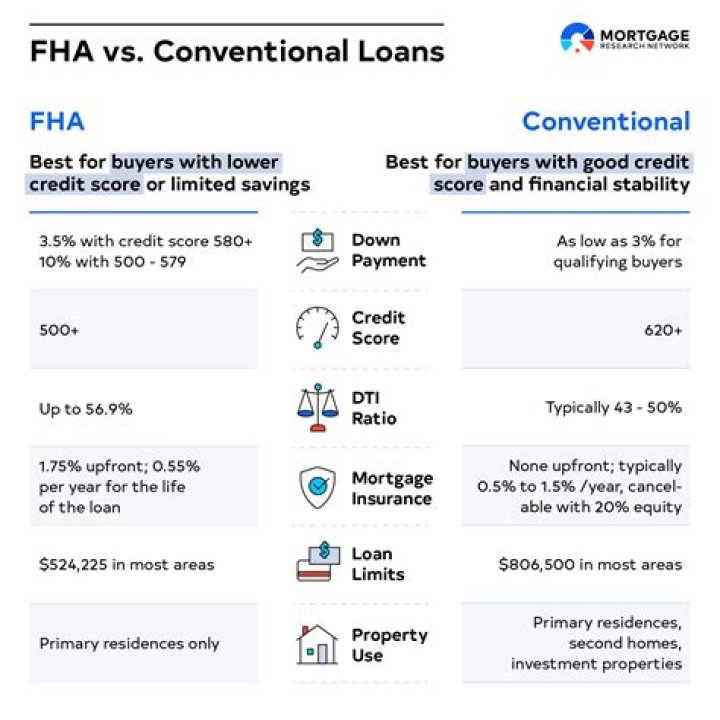

Why is FHA better than conventional?

FHA loans allow lower credit scores than conventional mortgages do, and are easier to qualify for. Conventional loans allow slightly lower down payments. … FHA loans are insured by the Federal Housing Administration, and conventional mortgages aren’t insured by a federal agency.

Does FHA require seller pay closing costs?

Help From Sellers FHA loans allow sellers to cover closing costs up to six percent of your purchase price. That can mean lender fees, property taxes, homeowners insurance, escrow fees, and title insurance. Naturally, this kind of help from sellers is not really free.

Why do FHA loans fall through?

If a borrower has insufficient funds to cover the down payment and/or closing costs, the FHA loan might fall through. Lenders usually discover this kind of issue on the front end, when the borrower first applies for a loan.

Can a mortgage lender pull out after closing?

Federal law gives borrowers what is known as the “right of rescission.” This means that borrowers after signing the closing papers for a home equity loan or refinance have three days to back out of that deal.

What can go wrong at closing?

Pest damage, low appraisals, claims to title, and defects found during the home inspection may slow down closing. There may be cases where the buyer or seller gets cold feet or financing may fall through. Other issues that can delay closing include homes in high-risk areas or uninsurability.

Is no news good news with underwriting?

When it comes to mortgage lending, no news isn’t necessarily good news. … Particularly in today’s economic climate, many lenders are struggling to meet closing deadlines, but don’t readily offer up that information.

Can a landlord evict you for no reason?

You may need to engage your landlord if the notice to vacate is lawful. The landlord cannot evict you for no reason – merely because they want you out. There are legal regulations guiding the termination of a lease agreement. … The law does not support your eviction into homelessness.

Can my landlord evict me?

Landlords can’t just lock you out, even if you are behind on rent. They must get a court judgment first. Your landlord can’t evict you without terminating the tenancy first. This usually means giving you adequate written notice, in a specified way and form.

Can an underwriter be held liable?

Conclusion. Banks and lenders should be relieved to know that they do not have a duty to perform reasonable loan processing or underwriting, and cannot be held liable for negligently processing or underwriting a loan.

Can you sue a mortgage company for taking too long?

Briefly, lender liability law says lenders must treat their borrowers fairly, and when they don’t, they can be subject to borrower litigation under a variety of legal claims. The decade-long evolution of lender liability has resulted in most cases now involving breach of contract and/or fraud claims.

Why do title companies have Underwriters?

An underwriter is someone that authorizes its agents to write title insurance policies. They are the ones who assume the financial risk and ensure the property against insurable defects. If any undiscovered legal issues ever arise, a title insurance underwriter will defend the power of the title policy.

Can a seller contest an appraisal?

Either the buyer or the seller can challenge an appraisal or request a second appraisal. “A challenge should be based on specific errors rather than opinions,” notes Stephens.

Can you refuse appraisal?

You are not legally required to sign a performance appraisal nor will you be threatened with legal action if you refuse to sign your performance appraisal. However, if you do refuse, your supervisor or an HR staff member will probably indicate on the signature line that you refused to sign.

Why would FHA require a 2nd appraisal?

HUD has instituted the possibility of a second appraisal when applying for a Reverse Mortgage loan. If the FHA feels the original appraisal is inadequate or deficient, a second appraisal from a new appraiser is ordered.

Can a seller cancel a contract?

Without a valid reason to terminate a contract, the seller can only get out of the sale legally if the buyer releases them. There are two ways this typically happens: More common: The buyer backs out using one of their contingencies. Less common: Both parties mutually agree to cancel the contract.

How accurate is zestimate?

How Accurate is Zestimate? According to Zillow’s Zestimate page, “The nationwide median error rate for the Zestimate for on-market homes is 1.9%, while the Zestimate for off-market homes has a median error rate of 7.5%. … For homes in LA, the Zestimate was fairly accurate – hovering close to -5% for all homes.